Hey guys, this is Alan Moore, a certified financial planner and founder of Serenity Financial Consulting. Thanks for joining me. So, you want to contribute to a Roth IRA, but you've been told you make too much money, huh? If you make more than $110,000 in adjusted gross income (or $173,000 if you're married) for 2010, you can't contribute directly to a Roth IRA because of the income limitations. But you still really want to contribute to a Roth IRA, right? Well, there is a way – it's called non-deductible IRA contributions. Non-deductible IRA contributions are essentially contributions that are made into a traditional IRA that you don't take a tax deduction for. With a traditional IRA, you normally put money in, take a tax deduction in the current year, the money grows tax-deferred, and when you take it out in retirement, it's all taxable at your income rate in retirement. A Roth IRA, on the other hand, allows you to put money in, pay the taxes when you put it in (no tax deduction), and it grows tax-free. The non-deductible IRA is kind of somewhere in the middle. You don't get to take the tax deduction for your contribution, but the growth is allowed to grow tax-deferred. However, you have to pay taxes on the growth in retirement. Now, if we had a way of turning a non-deductible contribution into a Roth contribution, it would be a huge tax savings because essentially you would never have to pay tax on the growth within that account. And if you think about it, getting six, seven, eight percent of growth per year over the next 30-40 years until you need that money, that's a huge amount of taxes. Well, there is a way to do this, and here's what you have...

Award-winning PDF software

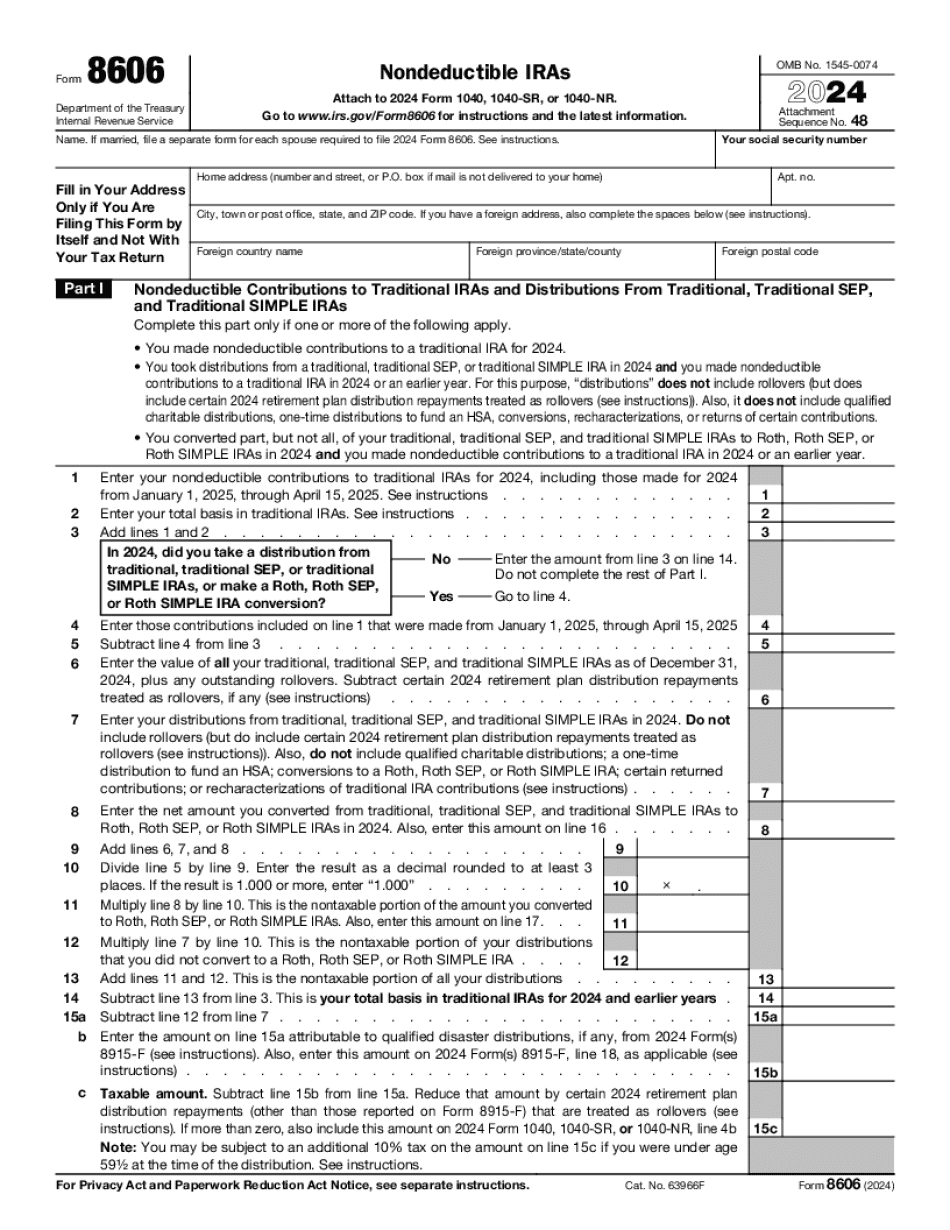

8606 basis Form: What You Should Know

Taxpayers must report nondeductible contributions that exceed their annual contribution limit in 2025 or 2019. IRAs are tax-deferred accounts, so this is also a time when you can deduct contributions from the year in which they are made. (You can deduct your prior year's contributions.) However, deductions from the current year cannot be claimed until the following year. There are two ways of deducting your nondeductible contribution. You can claim the deduction within the current year, or you can postpone using that deduction until the following year. However, if you make the nondeductible contribution before you have had a tax year in the current year, you will not be able to use that contribution. For example, if you make a nondeductible contribution in January and you have no tax year in 2025 or 2019, the contributions you made are not deductible until December 31, 2019. If you make a nondeductible contribution in January and you have a tax year in 2017, the contributions you made are deductible in June of the following year. (Note: If you do not make a nondeductible contribution in January, the contribution, even if it may be deducted in June, is not considered basis as of January 1. This means that you will be required to include the contribution to your income tax return for the year in which you make your contribution.) You can postpone the nondeductible contribution until the following year. For instance, if you make a nondeductible contribution in October, and you have a 2025 tax year, you can postpone the contribution until June. This means that the contribution, even if it has an exclusion of over 50,000 for 2017, will be included for the tax year in which you make it. The following table lists the timing requirements for both methods. Example 1 : If a taxpayer makes a nondeductible contribution in January that is not deductible in January, or a contribution in November that is not deductible in November, the contribution is included in the tax years 2017, 2025 and 2019. Example 2 : If a taxpayer makes a nondeductible contribution in October that is not deductible in October or a contribution in November that is not deductible in November, the contribution is included in the tax years 2017, 2025 and 2019. Example 3 : Both a contribution in January and a contribution in November that would have been deductible in January are included in 2017. Example 4 : Only a contribution for 2025 is included in future years without a deduction for 2018.

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 8606, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 8606 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 8606 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 8606 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Form 8606 basis