Award-winning PDF software

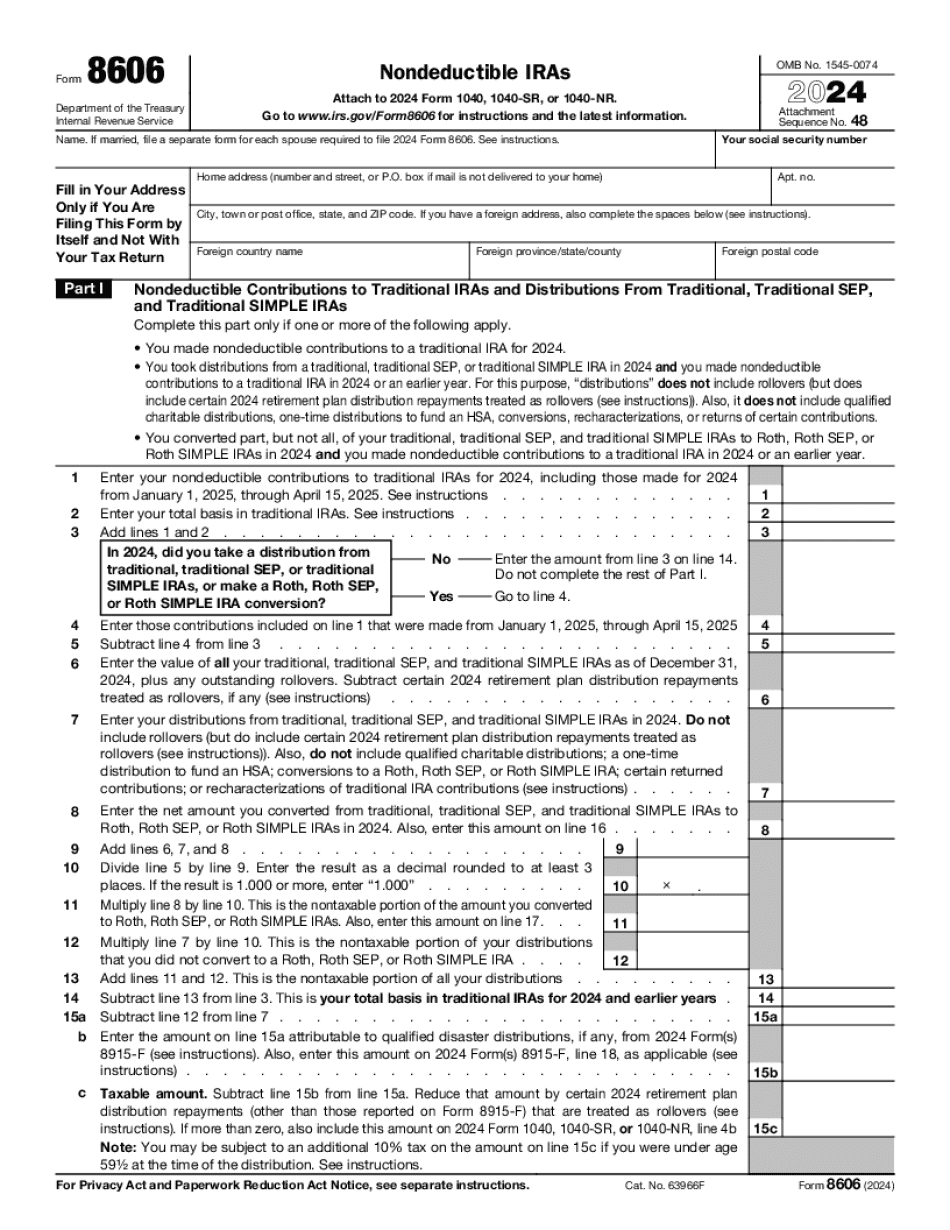

Form 8606 Minnesota: What You Should Know

PDF, IRA Disallowed Contribution — IRS). IRS Form 2106, Special Withholding Tax for Non-Qualified Deferral or Disqualified Distribution Mar 28, 2025 — No, in 2018, the IRS will not impose any separate tax on qualified distributions to a non-qualified plans, which means that if the distribution to the plan is from a qualified plan then it is not subject to taxation. Qualified distributions are distributions from qualified plans, and the qualified employee can take part of the distribution without penalty. IRS Form 4868A, Statement of Tax Effect on Excess Distribution or Withholding June 13, 2025 — No, the IRS can accept and use in any year information from you (or someone you've authorized) that confirms that when the individual took the distribution from the plan that the individual was a plan participant. However, you are unable to attach a copy of the Form 4868 to your federal income tax return. Sep 14, 2025 — No, the IRS will not adopt a rule change to the IRS Form 4973 that would eliminate reporting on Form 4868 when you receive an individual's qualified distribution from a traditional IRA, a SEP, a SIMPLE IRA, or a catch-up 401(k) that's includable in gross income under the limitations set by Sec. 402(q)(2). Form 4973 for individuals electing to be treated as making election within the calendar year of the distribution for purposes of claiming the maximum elective deferral deduction for that year, and Form 2106 for other investors with regard to distributions from 401(k) plans Jan 1, 2025 — No, an individual's taxable income will be reduced for any year before the year of the distribution (e.g., if you receive a distribution in 2019, you have an income tax deduction to make with respect to the distribution in 2019) by any tax withheld on the plan distributions of the year before the year in which the distribution is received. In all other respects, the income tax will be the same as if the distribution had been received in the year that it is received. IRS Form 4868A, Statement of Tax Effect on Excess Distribution or Withholding May 26, 2025 — No, the IRS can accept and use in any year information from you (or someone you've authorized) that confirms that when the individual took the distribution from the plan that the individual was a plan participant.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Form 8606 Minnesota, keep away from glitches and furnish it inside a timely method:

How to complete a Form 8606 Minnesota?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Form 8606 Minnesota aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Form 8606 Minnesota from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.